Copay Card Deductible Calculator

How Copay Cards Actually Work

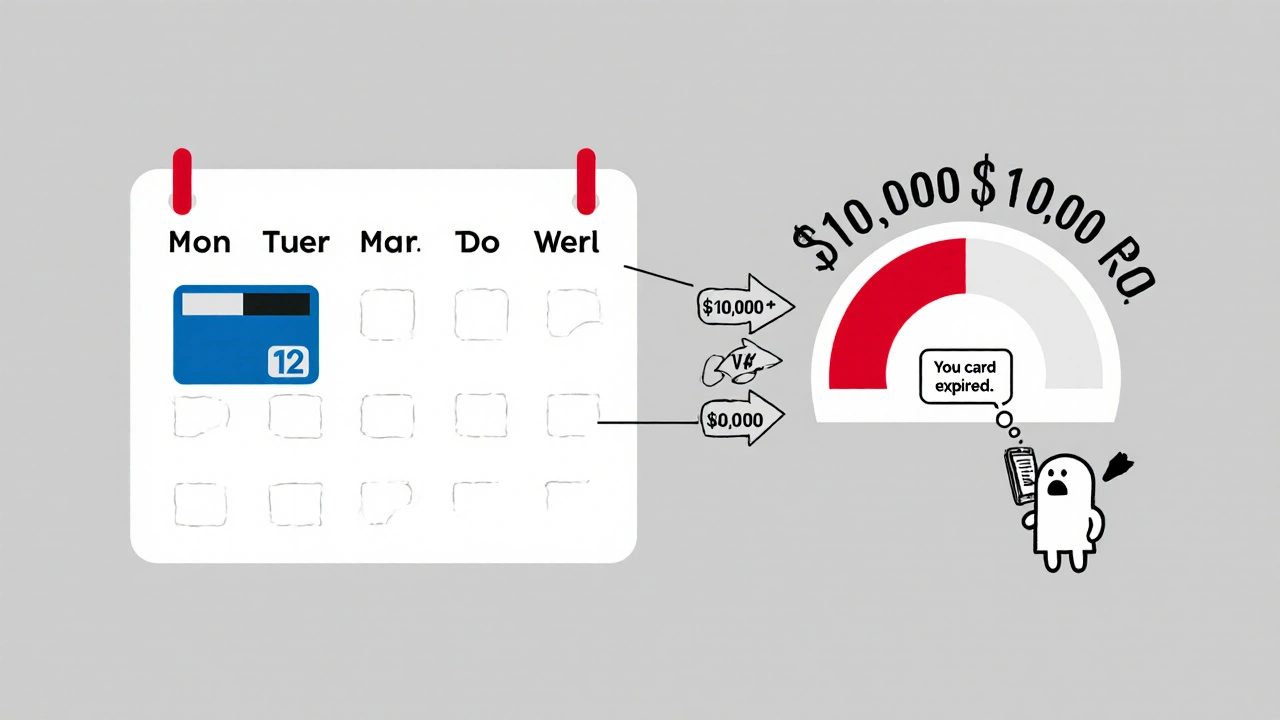

This calculator shows you how copay card payments impact your deductible progress. Remember: many insurers don't count copay card payments toward your deductible. Your actual progress may be slower than you think.

Deductible Progress Summary

Deductible Progress with Copay Card:

(This may NOT count toward your deductible)

Actual Deductible Progress (if card doesn't count):

(Only your insurance payments count)

Action Steps

- 1. Call your insurer: Ask: "Does my plan count copay card payments toward my deductible?"

- 2. Check your deductible progress: Log into your insurance portal monthly

- 3. Set a calendar alert: 6 months before card expiration, contact your drug manufacturer for assistance

- 4. Ask your pharmacy: "Do you offer accumulator alerts when my card has 20% left?"

When you’re managing a chronic condition like multiple sclerosis, rheumatoid arthritis, or Crohn’s disease, your medication isn’t just a pill-it’s your lifeline. But when that pill costs $7,000 a month, even with insurance, you’re stuck. That’s where copay cards come in. They seem like a gift: swipe them at the pharmacy, and your monthly bill drops from thousands to just a few dollars. But here’s the catch-what happens when that card runs out? And did your insurance even let those payments count toward your deductible? If you don’t know the answer, you could be one payment away from having to stop your treatment.

What Copay Cards Really Do (And Don’t Do)

Copay cards are offered by drug manufacturers to help commercially insured patients pay for expensive specialty drugs. They’re not free money. They’re a bridge. If your drug costs $8,000 a month and your insurance says you pay $1,500, the card might cover $1,400 of that, leaving you with $100. Sounds great, right? But here’s what no one tells you: that $1,400 might not count toward your deductible or out-of-pocket maximum. That’s because most large insurers now use something called a copay accumulator program. Since 2016, companies like UnitedHealthcare, Cigna, and Aetna have quietly changed how they handle manufacturer assistance. Instead of letting the card’s payment reduce your deductible, they treat it like a gift card you can’t spend on your own costs. Your deductible stays at $7,000-even if you’ve paid $10,000 out of pocket thanks to the card. You’re paying more, and you’re getting nowhere closer to insurance coverage.The Hidden Trap: When Your Card Runs Out

The real danger isn’t the cost of the card-it’s what happens after it expires. Most cards last a year, sometimes two. Patients assume that after paying $100 a month for 12 months, they’re almost done with their deductible. But if the card payments never counted, you’re still at zero. When the card stops, your bill jumps from $100 to $7,000 overnight. No warning. No grace period. Just a phone call from the pharmacy saying, “We can’t process this.” A 2023 NIH study found that 23.4% of patients on specialty medications stopped treatment after their copay card ran out. That’s not a mistake. That’s a system failure. One patient on Reddit shared: “I used my card for two years. My out-of-pocket was $10 a month. When it expired, I had to choose between my medicine and rent. I chose rent.”How Accumulator Programs Work (And Why They’re Risky)

Here’s how it breaks down:- Traditional copay assistance (pre-2016): Manufacturer payments counted toward your deductible and out-of-pocket maximum. You paid less, and you got closer to full coverage.

- Copay accumulator programs (now in 56% of commercial plans): Manufacturer payments are ignored. You pay the full cost of your drug, but only your own money counts toward your deductible. You’re paying more, and getting nowhere.

- Copay maximizer programs (used by 42% of large insurers): The insurer sets your copay to exactly match the maximum the card can cover. You pay $0-but your deductible doesn’t move. You’re stuck paying $0 until the card runs out, then hit with the full cost.

Who Gets Left Out?

Copay cards aren’t for everyone. Federal law bans them for people on Medicare or Medicaid. That means if you’re over 65, on disability, or rely on state assistance, you’re on your own. Even if you have private insurance, some plans don’t allow copay cards at all. And if you’re on a high-deductible health plan (HDHP), you’re the most vulnerable. You’re already paying more upfront. Without the card counting, you’re trapped.How to Use Copay Cards Safely

You can’t avoid copay cards if you need them. But you can protect yourself. Here’s how:- Ask before you use it: Call your insurance company and ask: “Do you have a copay accumulator or maximizer program for my medication?” Don’t rely on the pharmacy. They won’t always know.

- Check your deductible progress: Log into your insurance portal every month. Look at how much of your deductible you’ve met. If it hasn’t moved, your card payments aren’t counting.

- Know the expiration date: Most cards expire after 12 months. Mark your calendar. Six months before it runs out, start asking: “What happens next?”

- Talk to your specialty pharmacy: Many now offer “accumulator alerts.” If your card has 20% left, they’ll warn you and help you find alternatives.

- Ask about patient assistance programs: If your card runs out, the manufacturer might still help. Some offer free drug programs for low-income patients, even if you’re insured.

What’s Changing in 2025 and Beyond

There’s some good news. In September 2024, the Department of Health and Human Services proposed a new rule: insurers must clearly explain accumulator programs during enrollment and send monthly statements showing your true deductible progress. That rule takes effect January 1, 2026. It won’t fix everything, but it forces transparency. Some insurers are also starting to offer “transparency dashboards” that show you exactly how much you’ve paid and what counts. CVS Caremark rolled one out in April 2024-but only for 28% of their members. That’s not enough. Meanwhile, Congress is considering the Copay Accumulator Moratorium Act. Introduced in 2023, it would ban these programs for three years while experts study their impact. With 72 bipartisan co-sponsors, it’s gaining traction. But drug companies spent $28.7 million lobbying against it in early 2024. The fight isn’t over.

Real Stories, Real Consequences

A patient with lupus told her doctor: “I’ve been paying $10 a month for 18 months. I thought I was almost done. Now I have to pay $7,000? I can’t do this.” She stopped her meds. Her kidneys started failing. She spent six weeks in the hospital. Her total cost? $140,000. With the card counting, she’d have paid $1,200. Another patient, with rheumatoid arthritis, used his card for two years. When it expired, he called his insurer. They said, “You’ve paid $24,000, but your deductible is still $6,000.” He couldn’t believe it. He had to switch to a cheaper drug. It didn’t work. He lost mobility in his hands. These aren’t rare cases. They’re the new normal.What You Can Do Right Now

If you’re using a copay card:- Call your insurer today. Ask about accumulator programs.

- Download your monthly statements. Track your deductible progress.

- Set a reminder: 6 months before your card expires, start planning.

- Ask your pharmacist: “Is there another program I can qualify for when this ends?”

- Join a patient advocacy group. They track these changes and can help you fight back.

Do copay cards count toward my deductible?

Usually not-if your insurance plan uses a copay accumulator program. These programs, now used by over half of commercial insurers, treat manufacturer payments as external assistance that doesn’t count toward your deductible or out-of-pocket maximum. Always check with your insurer directly. Don’t assume it’s counting.

Who can use copay cards?

Only people with private, commercial insurance. Copay cards are illegal for Medicare, Medicaid, and other government-funded programs due to federal anti-kickback laws. If you’re on Medicare or Medicaid, you may qualify for separate patient assistance programs offered by drug manufacturers.

What’s the difference between an accumulator and a maximizer program?

An accumulator program ignores manufacturer payments entirely-they don’t count toward your deductible. A maximizer program sets your copay to exactly match the maximum the card can cover, so you pay $0-but your deductible still doesn’t move. Both keep you from reaching your out-of-pocket maximum faster, but maximizers make you think you’re paying nothing, which can be more misleading.

How do I know if my plan has an accumulator program?

Call your insurance company and ask: “Do you have a copay accumulator or maximizer program for my specific medication?” You can also check your Summary of Benefits and Coverage (SBC) document, though they’re often vague. Look for phrases like “manufacturer coupons do not apply to deductible/out-of-pocket maximum.”

What should I do when my copay card expires?

Start planning 6 months before expiration. Contact the drug manufacturer to ask about free drug programs or long-term assistance. Talk to your specialty pharmacy-they may have access to alternative funding. If your deductible hasn’t been met, you may need to switch to a less expensive medication or appeal your insurance coverage. Don’t wait until the last minute.

james thomas

November 26, 2025 AT 19:55