When your doctor prescribes a brand-name medication but your insurance says you must switch to a cheaper generic version - and you know it won’t work for you - you’re not alone. Thousands of people face this every year. Insurance companies use formularies and step therapy rules to cut costs, but sometimes those rules ignore real medical needs. The good news? You can fight back. And if you do it right, you have a very good chance of winning.

Why Your Insurance Might Deny Your Medication

Insurance plans don’t just randomly say no. They follow strict rules called formularies, which list which drugs they cover and under what conditions. Many plans require you to try cheaper generics first - this is called step therapy. If that fails, you might be allowed to move up to the brand-name drug. But if your doctor says the generic won’t work - maybe because you had bad side effects, or it doesn’t control your condition - you need to appeal.Denials happen for a few common reasons:

- You didn’t try the required generic or lower-cost drug first

- The insurer says there’s no proof the brand-name drug is medically necessary

- Your doctor didn’t fill out the right forms

- The appeal was submitted too late

But here’s what most people don’t know: 72% of these denials get overturned when the appeal is properly documented. That’s not luck. That’s process.

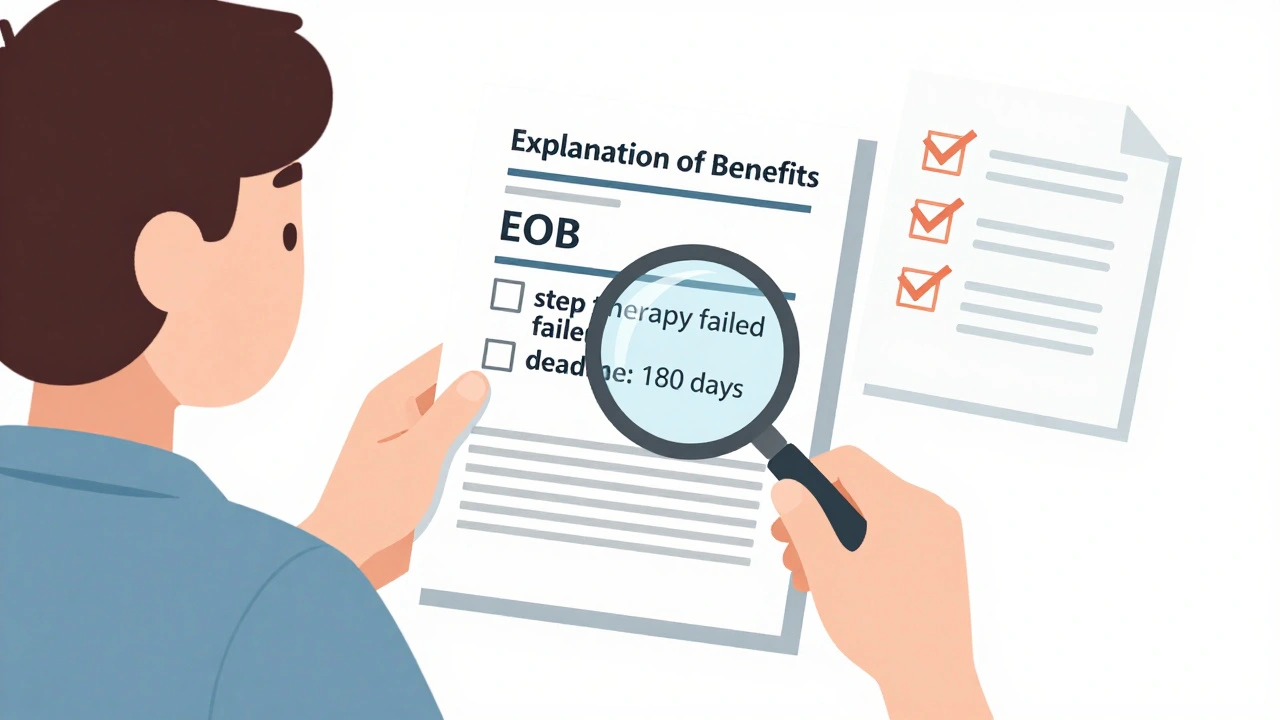

Step 1: Read Your Explanation of Benefits (EOB)

The first thing you need is your EOB - the document your insurer sends after denying coverage. It’s not just a bill. It’s your roadmap. Look for:- The exact reason for denial

- The name of the medication that was denied

- Which step therapy requirement you supposedly didn’t meet

- How to file an appeal - and the deadline

By federal law, insurers must include this info. If it’s missing, call them. Don’t wait. You have 180 days from the denial date to file an internal appeal for most commercial plans. Medicare gives you only 120 days. Miss the window, and you lose your right to appeal.

Step 2: Get a Letter of Medical Necessity from Your Doctor

This is the most important step. No appeal wins without it.Your doctor needs to write a letter explaining why the brand-name drug is necessary - not just preferred. The letter must include:

- Specific clinical reasons why the generic won’t work (e.g., “Patient experienced severe rash and anaphylaxis with generic levothyroxine”)

- Proof of prior treatment failures - list every generic or alternative tried, when, and what happened

- References to official guidelines - like those from the American College of Physicians or the American Diabetes Association

According to a GoodRx analysis of 15,000 appeals, 78% of successful appeals included a letter citing clinical guidelines. Only 29% of failed appeals did.

Doctors hate paperwork. But if you give them a template, they’re more likely to help. Here’s what to ask for:

“Please write a letter stating that [Medication Name] is medically necessary because [specific reason]. I have tried [List generics] and experienced [side effects or lack of effectiveness]. This is supported by [guideline name, e.g., ADA 2023 Standards].”

Step 3: Fill Out the Official Appeal Form

Your insurer will have a form - often called a “Prior Authorization or Step Therapy Exception Request.” Don’t skip this. Even if you have a great letter, the form is required.Make sure you include:

- Your full name and insurance ID number

- Exact drug name and dosage

- Prescribing doctor’s name and NPI number

- Date of denial

- Copy of the doctor’s letter

Some states have specific forms. In California, AB 347 requires insurers to accept physician documentation as sufficient for step therapy exceptions. In New York, peer-to-peer reviews must happen within 72 hours. Check your state’s insurance department website for rules.

Step 4: Submit Everything - and Keep Copies

Send your appeal via certified mail or online portal - never just a phone call. Email or fax can get lost. Certified mail gives you proof of delivery.Insurers have deadlines too:

- Standard appeals: 30 days if you haven’t started the drug, 60 days if you’re already taking it

- Expedited appeals: 4 business days if your condition is urgent (e.g., risk of hospitalization, worsening disease)

If your doctor says you need the drug right away, mark your appeal as “expedited.” Include a note: “Patient’s condition will deteriorate without immediate access to [drug name].”

Step 5: If Denied Again - Go External

If your insurer says no again, you’re not done. You have the right to an external review by an independent third party.This is where things get powerful. For Medicare Part D, the second level of appeal - handled by an Independent Review Entity - has a 63.2% success rate. For commercial plans, external reviewers overturn denials in about 56-78% of cases when documentation is solid.

To start this step:

- Call your insurer and ask for the external review request form

- Submit your original appeal package again - plus any new evidence

- Request a peer-to-peer review: your doctor speaks directly to the insurer’s medical director

Studies show peer-to-peer calls have a 75%+ success rate. The insurer’s doctor hears the real clinical reasoning - not just paperwork. It’s often the turning point.

What Works - And What Doesn’t

Not all appeals succeed. Here’s what separates winners from losers:| Successful Appeals | Failed Appeals |

|---|---|

| Doctor’s letter cites specific clinical guidelines | Generic reason like “I feel better on this one” |

| Proof of 2+ failed alternatives | Only tried one generic |

| Submitted within deadline | Missed the 180-day window |

| Peer-to-peer review requested | Only patient wrote the appeal |

| Used certified mail or online portal | Relied on phone calls or emails |

One patient with Type 1 diabetes successfully appealed denial of semaglutide after showing three prior episodes of dangerous hypoglycemia with other drugs. Her doctor attached lab results and endocrinology guidelines. Approved in 11 days.

Another patient with Crohn’s disease had 11 denials before winning. Why? Because every time, they added a new failed drug and updated the letter. Persistence with documentation wins.

When to Call Your State Insurance Commissioner

If your appeal drags on, or you get conflicting info, contact your state’s insurance department. In California, they resolve 92% of formal complaints within 30 days. Most states have free consumer advocacy offices.They can:

- Force your insurer to respond

- Clarify your rights under state law

- Fast-track your case if it’s urgent

Don’t wait until you’re desperate. Call early. The average response time is under a week.

Common Mistakes to Avoid

Here’s what kills appeals before they start:

- Waiting too long to act - deadlines are strict

- Letting the pharmacy handle the appeal - they don’t know your medical history

- Using vague language like “my doctor thinks this is better” - be specific

- Not including your insurance ID or policy number

- Assuming a generic is “just as good” - it’s not always true

One Johns Hopkins study found 41% of failed urgent appeals were denied because the request was mislabeled as “standard.” Always double-check the box.

What to Do If You Can’t Afford the Drug While Waiting

Appeals take time. You might need the drug now. Options:- Ask your doctor for samples

- Check patient assistance programs from drug manufacturers (e.g., RxAssist.org)

- Use GoodRx or SingleCare coupons - sometimes cheaper than insurance copay

- Apply for Medicaid or state pharmaceutical assistance programs

Don’t stop taking your meds because of a denial. Talk to your doctor about temporary solutions.

Final Thoughts: This Is Your Right

Insurance companies aren’t trying to hurt you. They’re following rules designed to save money. But those rules don’t always fit real lives. You have the right to safe, effective treatment. The appeals system exists for a reason - and it works when you use it right.Don’t give up after one no. Document everything. Get your doctor on your side. Follow the steps. And remember: over 70% of denials are reversed when people fight back properly.

Can I appeal if my insurance says the generic is just as good?

Yes. Insurance companies often assume generics are interchangeable, but that’s not always true. If you’ve had side effects, allergic reactions, or the generic didn’t control your condition, your doctor can document why the brand-name drug is medically necessary. Studies show 68% of overturned appeals involve documented adverse reactions to generics.

How long does an insurance appeal take?

Standard appeals take 30 to 60 days, depending on whether you’re already taking the medication. Expedited appeals for urgent cases must be decided in 4 business days. External reviews can take 30-45 days. Most successful appeals are resolved within 52 days on average, according to patient reports.

Do I need a lawyer to appeal?

No. Most people win without legal help. The key is documentation - not legal jargon. A clear letter from your doctor, filled-out forms, and following deadlines are what matter. You can call your state insurance commissioner for free help if you get stuck.

What if my doctor won’t help with the appeal?

Talk to them again. Many doctors don’t realize how critical their letter is. Bring them a template and explain: “This is the only way I can get my medication.” If they still refuse, ask for a referral to another provider who’s willing to advocate. Some clinics have patient advocates on staff.

Can I appeal for any generic medication?

Yes - but success depends on medical justification. Appeals are most successful for specialty drugs like those for diabetes, autoimmune diseases, epilepsy, and mental health. For common meds like blood pressure or cholesterol, insurers are less likely to budge unless you have clear evidence of harm or ineffectiveness.

Will appealing affect my insurance rates?

No. Filing an appeal has no impact on your premiums, coverage, or future eligibility. It’s a protected right under the Affordable Care Act. Insurers cannot penalize you for exercising it.

David Brooks

December 8, 2025 AT 07:03